Coursera - Introduction to Computational Finance and Financial Econometrics

Coursera - Introduction to Computational Finance and Financial Econometrics

MP4 | AVC 243kbps | English | 960x540 | 30ps | 10 weeks | AAC stereo 128kbps | 3.91 GB

Genre: Video Training

Learn mathematical, programming and statistical tools used in the real world analysis and modeling of financial data. Apply these tools to model asset returns, measure risk, and construct optimized portfolios using the open source R programming language and Microsoft Excel. Learn how to build probability models for asset returns, to apply statistical techniques to evaluate if asset returns are normally distributed, to use Monte Carlo simulation and bootstrapping techniques to evaluate statistical models, and to use optimization methods to construct efficient portfolios.

You'll do the R assignments for this course on DataCamp.com, an online interactive learning platform that offers free R tutorials through learning-by-doing. The platform provides you with hints and instant feedback on how to perform even better. Every week, new labs will be posted.

Course Syllabus

Topics covered include:

Computing asset returns

Univariate random variables and distributions

Characteristics of distributions, the normal distribution, linear function of random variables, quantiles of a distribution, Value-at-Risk

Bivariate distributions

Covariance, correlation, autocorrelation, linear combinations of random variables

Time Series concepts

Covariance stationarity, autocorrelations, MA(1) and AR(1) models

Matrix algebra

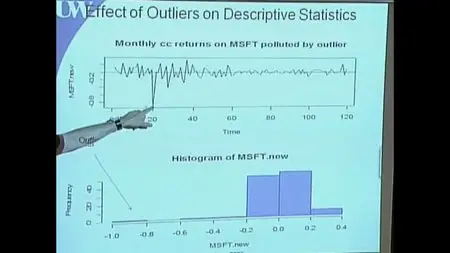

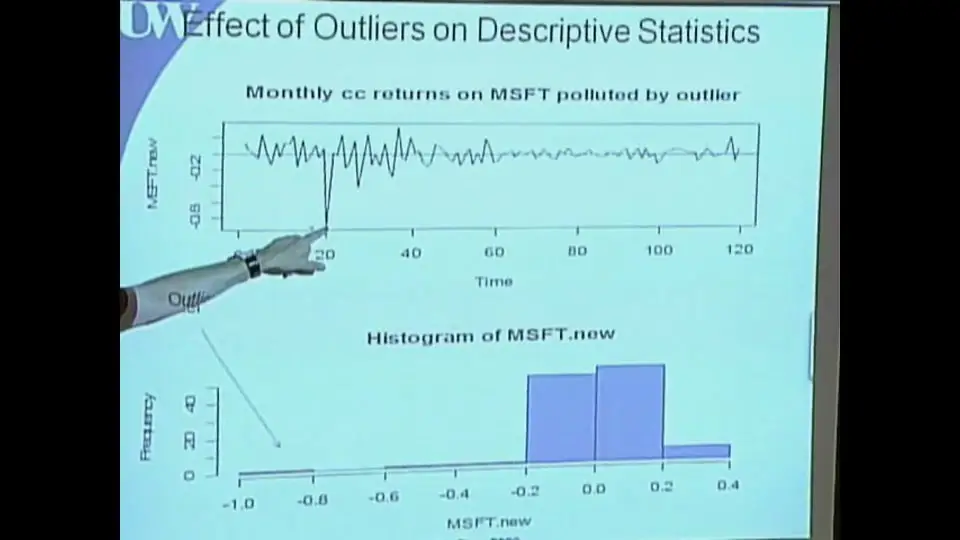

Descriptive statistics

histograms, sample means, variances, covariances and autocorrelations

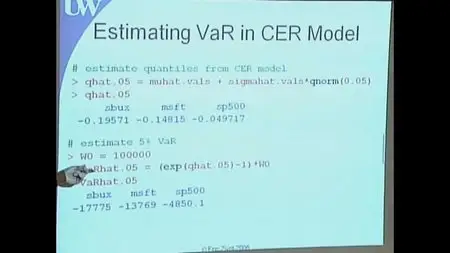

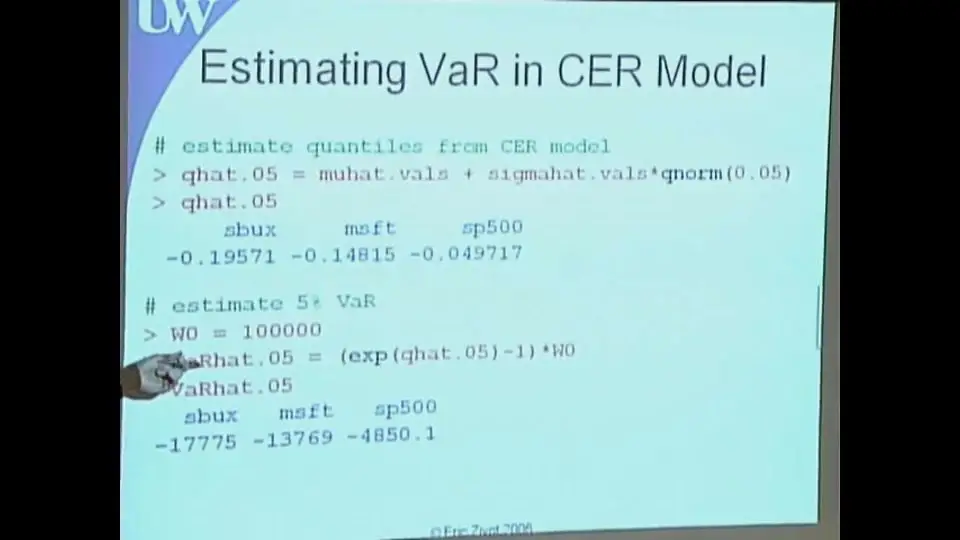

The constant expected return model

Monte Carlo simulation, standard errors of estimates, confidence intervals, bootstrapping standard errors and confidence intervals, hypothesis testing , Maximum likelihood estimation, review of unconstrained optimization methods

Introduction to portfolio theory

Portfolio theory with matrix algebra

Review of constrained optimization methods, Markowitz algorithm, Markowitz Algorithm using the solver and matrix algebra

Statistical Analysis of Efficient Portfolios

Risk budgeting

Euler’s theorem, asset contributions to volatility, beta as a measure of portfolio risk

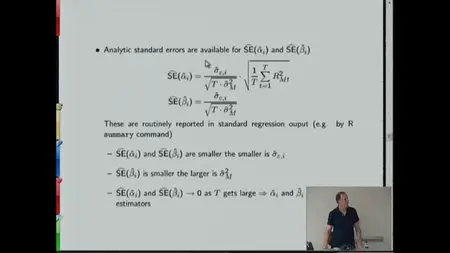

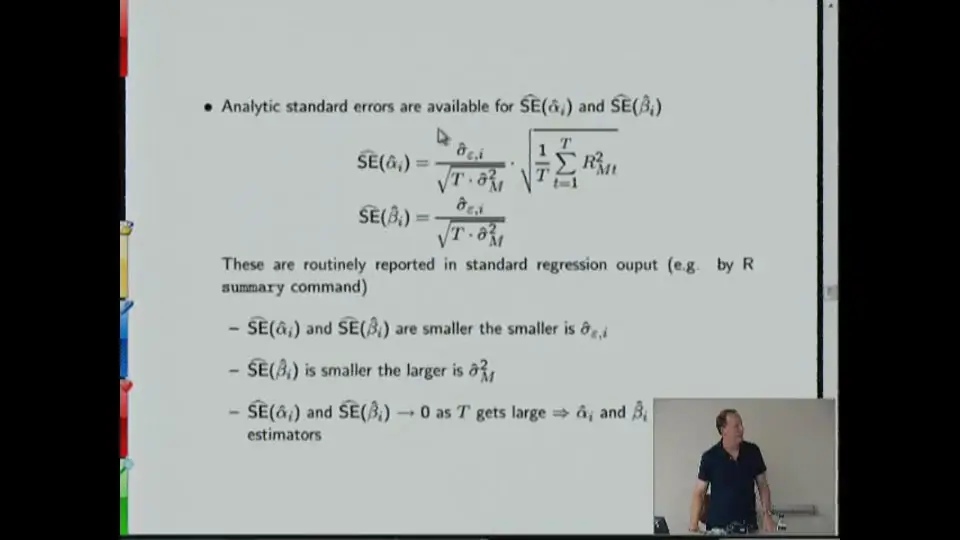

The Single Index Model

Estimation using simple linear regression

Coursera - Introduction to Computational Finance and Financial Econometrics

Coursera - Introduction to Computational Finance and Financial Econometrics

Coursera - Introduction to Computational Finance and Financial Econometrics

Coursera - Introduction to Computational Finance and Financial Econometrics

No mirrors please